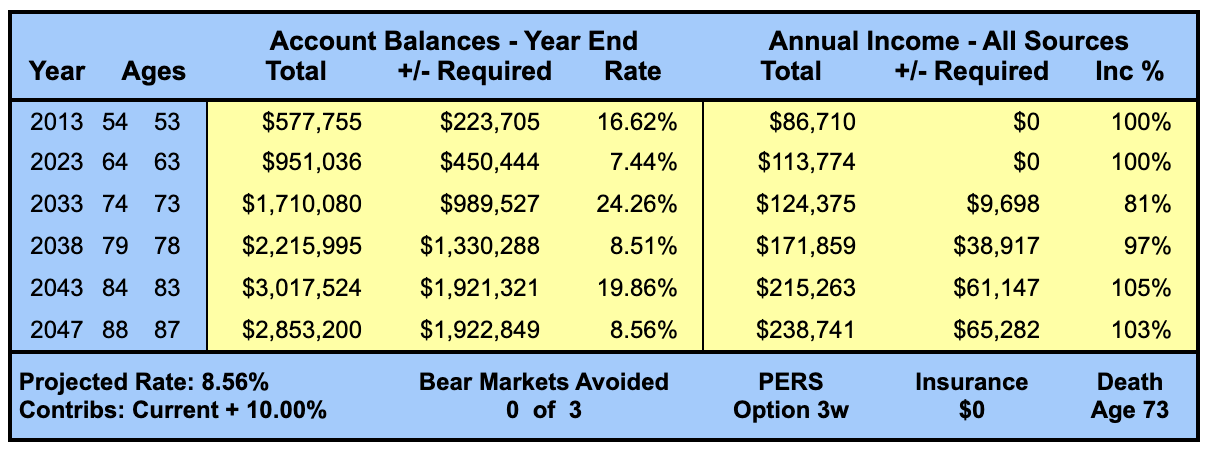

Main Scenario: Reasonable “Best Case” (Projections Over 35 Years).

Does your financial plan have enough built-in contingencies to weather the inevitable storms? If not, what PREVENTATIVE steps should you take? Here we tackle the two most serious concerns: (1) will UNEXPECTED stock market volatility - including severe BEAR MARKETS - jeopardize your financial plan? (2) If Richard dies, will the resulting loss of pension income reduce Carol's standard of living to UNACCEPTABLE levels?

Action Step: Evaluate the “Best Case” Scenario.

Here the investment results turn out BETTER than expected. But review the assumptions carefully: are they REASONABLE? If so, be prepared to take advantage of the "best case" scenario. Plan for the "worst" - but retain FLEXIBILITY and CONTROL over your planning choices.

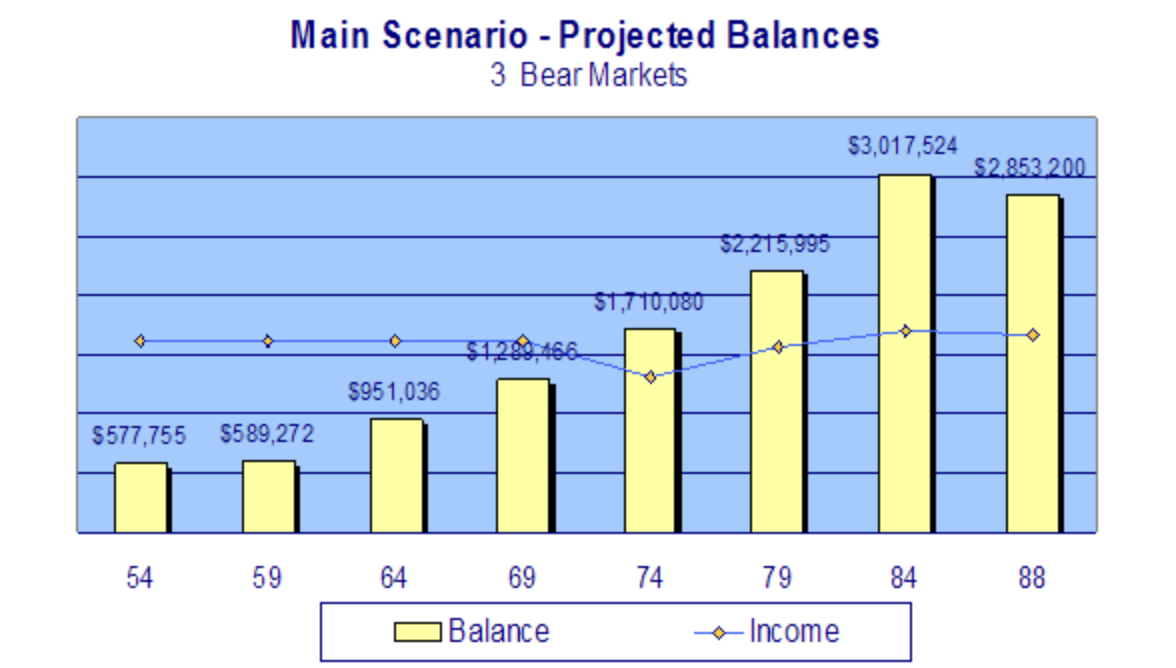

Main Scenario: “Best Case” Projected Balances.

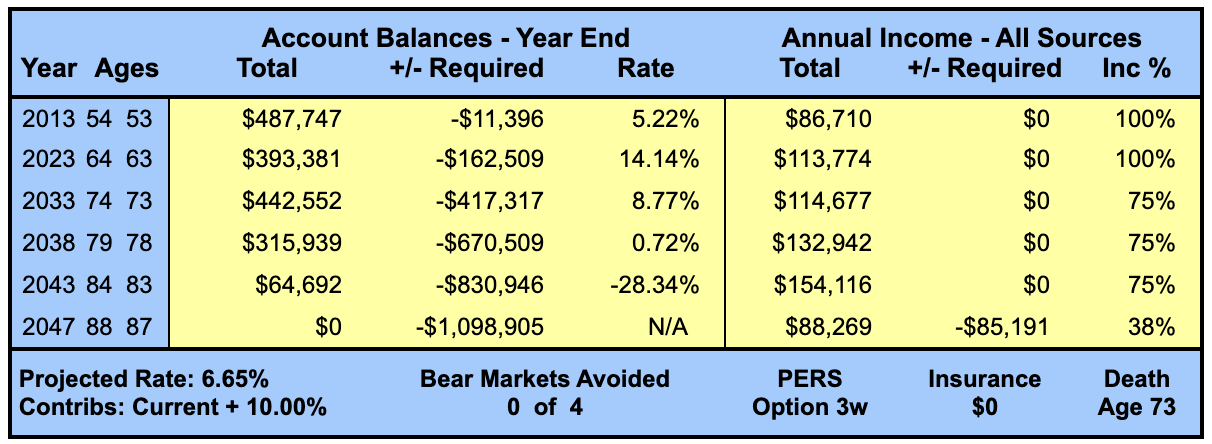

Main Scenario: Reasonable "Worst Case"

Main Scenario: Reasonable “Worst Case” (Projections Over 35 Years).

Volatility can wreck havoc on your financial plans. On the “surface” an average annual return of 6.65% appears adequate, but 4 severe bear markets (declines of 20% or more) over a period of 44 years have taken their toll.

By age 87, Carol’s retirement accounts are EXHAUSTED. Annual income is $85,191 LESS than required. Although expenses declined after Richard’s (hypothetical) death at age 73, Carol’s standard of living has been ravaged by inflation – and now equals only 38% of your pre-retirement income – clearly an UNACCEPTABLE level.

Anticipating potential problems (especially the “Worst Case” scenario) gives you more TIME to face the challenge. And with more time, you have more ways of fighting back.

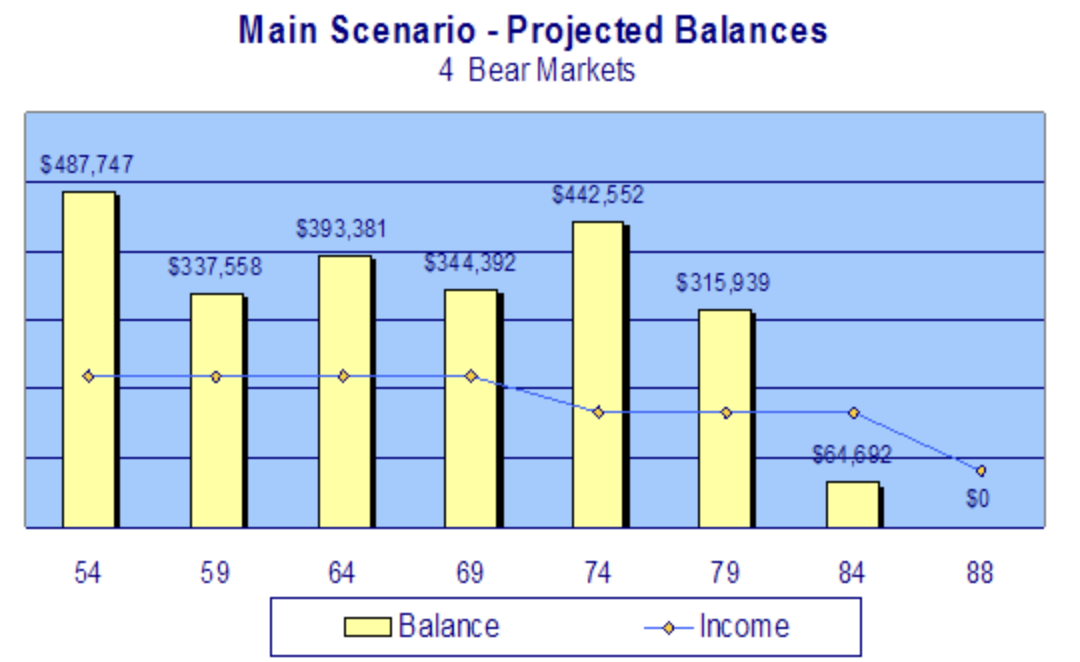

Main Scenario: “Worst Case” Projected Balances.