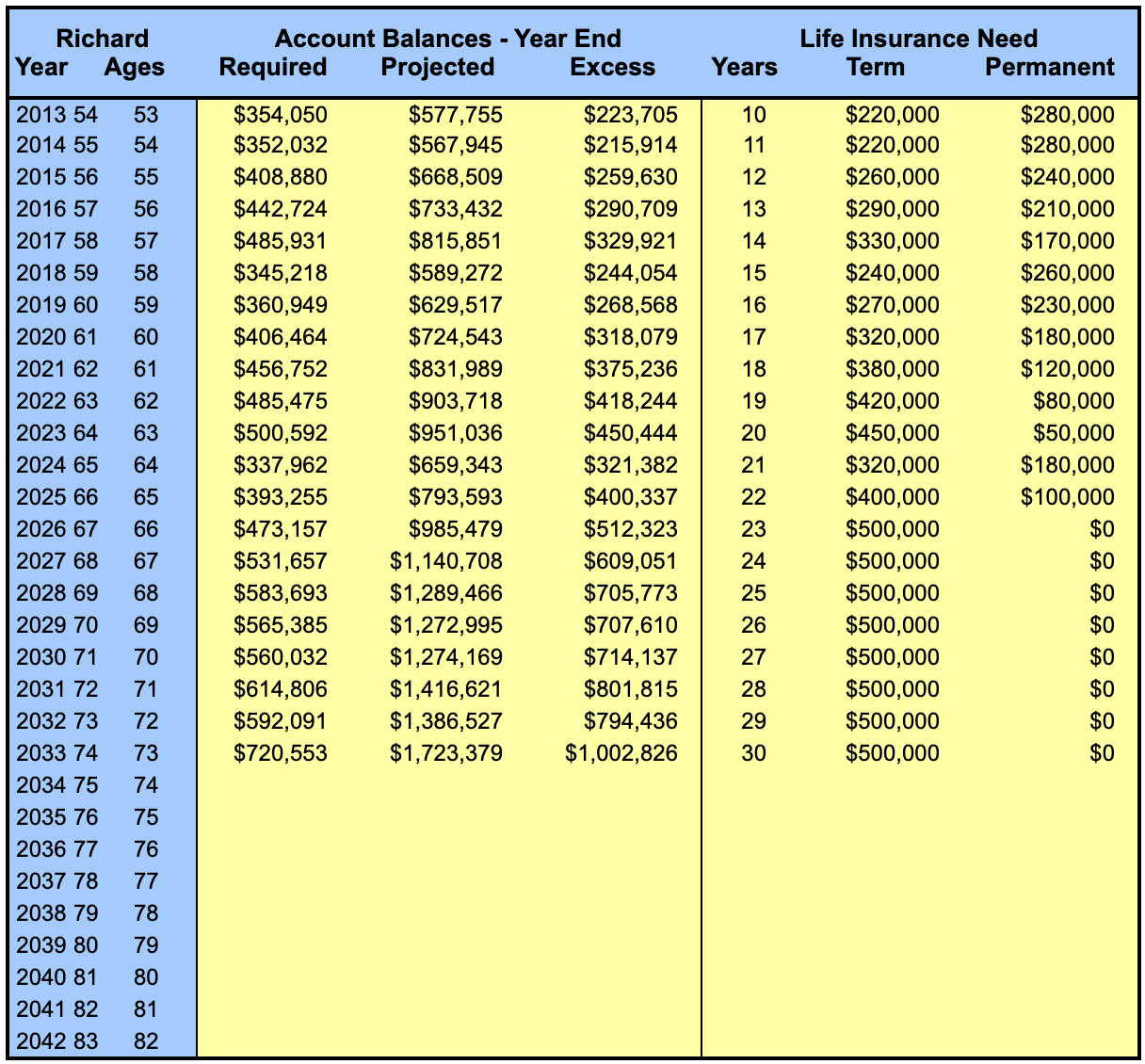

Main Scenario: Self-Insured Analysis (Richard: $500,000).

Protecting Richard's pension will require $500,000 of life insurance (when combined with OPTION 3W). But what TYPE of coverage should you have - Permanent or Term insurance?

Begin with a basic premise: "Self-Insurance" is NOT the amount you've saved - it's the amount your savings EXCEED what your plans REQUIRE. To the extent you can REASONABLY expect to become self-insured, you eliminate the need for PERMANENT insurance (and Survivor Options - which are another form of permanent insurance protection). TERM insurance, covering the period of years between now and your self-insured point, will be sufficient.

Based on your Self-Insured Analysis, Richard's optimal Life Insurance coverage is $500,000 of TERM insurance (30-Year).

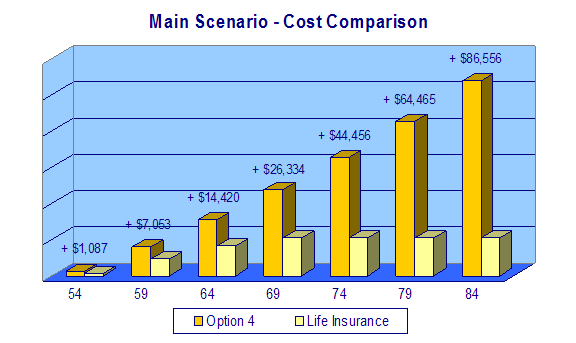

Main Scenario: Comparing Pension Protection Strategies

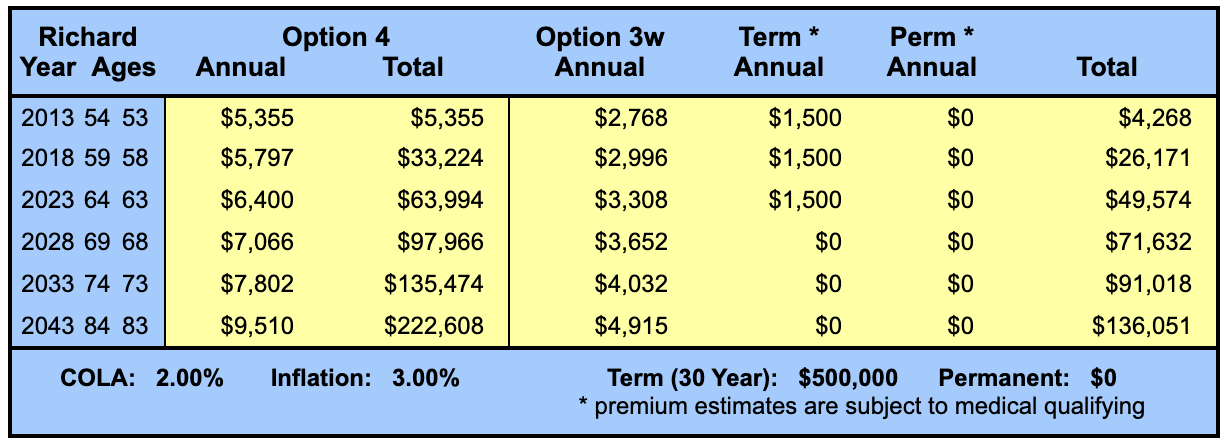

Main Scenario: Option 4 vs. Option 3w + Life Insurance.

Protecting Richard's pension requires a choice between two proven strategies: (1) using Survivor Options exclusively, OR (2) using a combination of Survivor Options and Life Insurance. Cost comparisons are important, especially when one strategy is substantially more expensive than the other. But understand the drawbacks of either choice: Survivor Options are irrevocable, inflexible, and rarely continue benefits to children. Life Insurance offers greater FLEXIBILITY and CONTROL, but how will the proceeds be invested? Will the income be reliable?

Action Step: Choose Your Pension Protection Strategy.